Discover how mortgage interest rates are determined. This guide reveals key factors, helping you understand rates and negotiate better deals.

Credit Bureau Mortgage Reporting: What Buyers Must Know

The role of credit bureau mortgage reporting is to supply lenders with accurate, comprehensive credit data that directly determines whether you qualify for a home loan and at what interest rate. The three major credit bureaus, Equifax, Experian, and TransUnion, each maintain separate records on your borrowing history. Because creditors are not required to report to all three, your file at each bureau can look meaningfully different. That gap matters more in mortgage lending than in almost any other credit decision you will make.

How does credit bureau reporting influence mortgage eligibility and rates?

Credit scores drive mortgage underwriting. Lenders use your score to place you in a pricing tier, and each tier carries a different interest rate. A score of 740 and a score of 719 can sit in different tiers, costing you thousands of dollars over the life of a loan.

The variance between bureaus is not trivial. Score differences across bureaus affect 35% of consumers by 10 or more points from the tri-merge average. That spread is enough to shift your eligibility or push you into a higher rate bracket. For borrowers near a pricing threshold, the difference between bureaus is the difference between approval and denial.

The financial stakes are concrete. A borrower with a $350,000 GSE loan at 90% LTV may see mortgage and insurance costs fluctuate by $3,000 to $5,000 due to credit score shifts between pricing tiers. That is not a rounding error. That is real money leaving your pocket because of how credit data is reported and interpreted.

Secondary market investors also rely on credit bureau data to price risk in mortgage-backed securities. When lenders sell loans to investors, those investors demand confidence in the underlying credit quality. Incomplete or inconsistent credit data raises risk premiums, which flows back to you as a borrower in the form of higher rates. Understanding how credit bureaus affect loans at this level gives you real leverage before you apply.

Key factors that credit bureau data influences in mortgage underwriting:

- Loan eligibility: Your score determines which loan programs you can access, including FHA, VA, and conventional products.

- Interest rate tier: Lenders price loans in bands. A score just below a threshold can cost you significantly more over 30 years.

- Private mortgage insurance (PMI) costs: Lower scores often trigger higher PMI premiums on loans with less than 20% down.

- Debt-to-income calculations: Lenders use bureau data to verify all reported debts, which feeds directly into your DTI ratio.

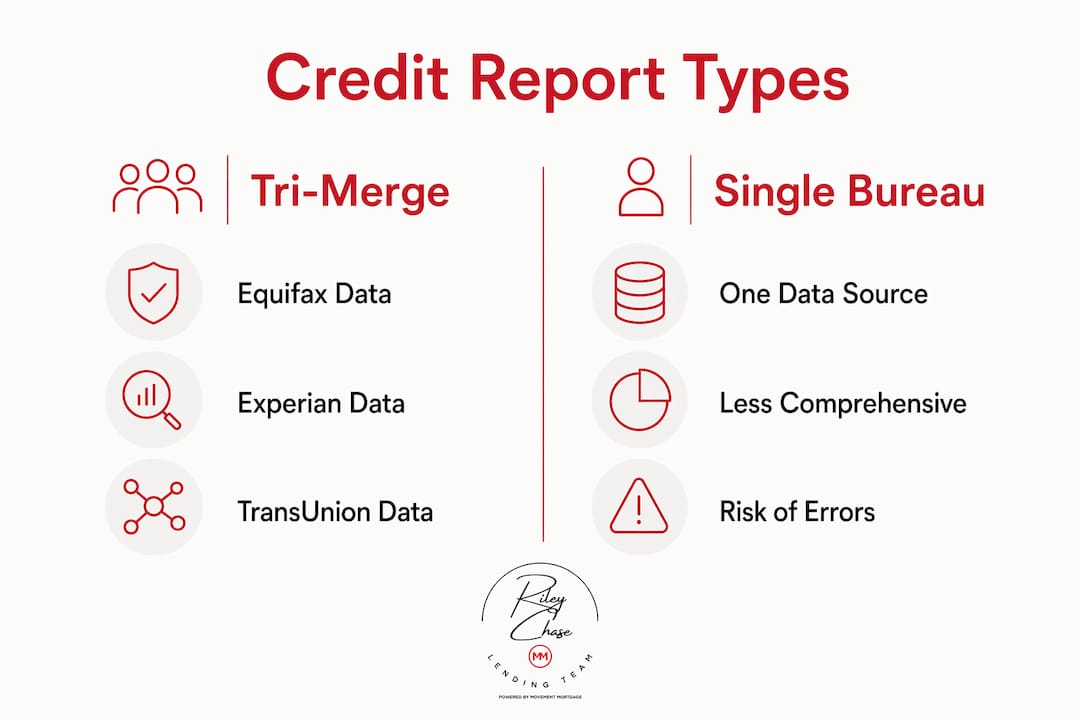

What is a tri-merge credit report, and why is it the mortgage standard?

A tri-merge credit report is not simply three credit reports stapled together. Tri-merge reports are algorithmically merged documents designed by credit reporting agencies to deduplicate tradelines and reconcile conflicts across all three bureaus. That distinction matters because the merging process removes duplicate accounts, flags inconsistencies, and produces a single, cleaner picture of your credit history.

The scoring method built into tri-merge underwriting adds another layer of stability. The median of the three bureau scores is the industry standard for mortgage qualification, chosen specifically to reduce the influence of outliers. If your scores are 710, 730, and 755, the lender uses 730. That middle number protects both you and the lender from a single bureau’s error or missing data pulling the decision in the wrong direction.

| Feature | Tri-merge report | Single bureau report |

|---|---|---|

| Data sources | Equifax, Experian, TransUnion | One bureau only |

| Tradeline deduplication | Yes, algorithmically merged | No |

| Score used | Median of three scores | Single score |

| Risk of missing data | Low | Higher |

| Secondary market acceptance | Standard | Not currently standard |

Pro Tip: Request your credit reports from all three bureaus at least 90 days before applying for a mortgage. That window gives you time to dispute errors and see your scores before a lender does.

The tri-merge approach also serves the broader mortgage market. Tri-merge remains the cornerstone of mortgage underwriting for regulatory compliance and risk mitigation, balancing the real differences that exist between bureau datasets. Investors who buy mortgage-backed securities depend on that consistency to price pools of loans accurately.

What are the risks of moving to single-bureau mortgage reporting?

The mortgage industry is actively debating whether lenders should be allowed to use a single credit bureau report instead of a tri-merge. Proponents argue it reduces costs and speeds up the process. The risks, though, are significant and fall partly on you as the borrower.

The core problem is missing data. Credit bureau datasets differ because creditors are not required to report to all three bureaus, which means a single bureau may simply not know about a debt or a derogatory mark that another bureau has on file. A lender relying on one bureau could approve a borrower who looks cleaner on paper than they actually are, or miss positive payment history that would have helped a different borrower qualify.

The rate impact is also measurable. Moving from tri-merge to single-file credit reports may increase mortgage rates by approximately 0.125% per 20-point score shift to offset increased risk. That premium gets built into the market because investors demand compensation for the uncertainty that comes with less complete data.

Risks that single-bureau reporting introduces for borrowers:

- Score shopping: Lenders or borrowers could select the bureau with the highest score, inflating credit quality metrics and masking real risk.

- Missed derogatory data: A collection account reported only to one bureau disappears from the picture entirely.

- Pricing volatility: Secondary market investors face greater uncertainty, which they price into rates across the board.

- Reduced market liquidity: Approximately 240,000 GSE loans face possible denials amid shifts to a single-report framework, signaling how disruptive the change could be.

The debate is not settled. What is clear is that any shift away from tri-merge reporting changes the risk landscape for lenders, investors, and borrowers alike. Knowing what underwriting looks for helps you stay ahead of those changes.

How can you manage your credit reports before applying for a mortgage?

Proactive credit management is one of the most direct ways to improve your mortgage outcome. You have more control than most buyers realize, and the steps are straightforward.

-

Pull all three bureau reports. Monitoring credit reports across all three bureaus helps you detect discrepancies and errors before a lender does. Visit AnnualCreditReport.com to access your free reports from Equifax, Experian, and TransUnion.

-

Check for errors on each report separately. An account that appears correctly on one bureau may show a wrong balance or a false delinquency on another. Each bureau has its own dispute process, and you need to file separately with each one.

-

Pay down revolving balances. Credit utilization, the ratio of your balance to your credit limit, affects your score at each bureau independently. Reducing utilization below 30% on each card can lift scores across all three reports.

-

Avoid opening new accounts. New credit inquiries and new accounts lower the average age of your credit history. In the 90 days before applying, keep your credit profile stable.

-

Verify that positive accounts appear on all three bureaus. Some lenders and creditors only report to one or two bureaus. If a long-standing account with a perfect payment history is missing from one bureau, your median score could be lower than it should be.

Pro Tip: If you find a legitimate error, dispute it in writing with the specific bureau and include supporting documentation. Bureaus are required to investigate within 30 days under the Fair Credit Reporting Act.

Understanding your credit score requirements for a mortgage before you apply puts you in a much stronger position at the negotiating table.

Key Takeaways

Credit bureau mortgage reporting directly shapes your loan eligibility, interest rate, and total borrowing cost, making it the single most important financial record to understand before you apply.

| Point | Details |

|---|---|

| Tri-merge is the standard | Lenders use a merged report from all three bureaus, not three separate reports. |

| Median score drives decisions | The middle of your three bureau scores is used, protecting against outlier errors. |

| Score gaps cost real money | A 10-point difference across bureaus can shift your rate tier and cost thousands over the loan term. |

| Single-bureau risks are real | Moving away from tri-merge can hide derogatory data and raise rates for all borrowers. |

| Early monitoring pays off | Reviewing all three bureau reports 90 days before applying gives you time to fix errors. |

Why I think most buyers underestimate their credit reports

Most buyers I talk with check one credit score on a free app and assume they know where they stand. That single number is almost never what a mortgage lender sees. The tri-merge process pulls data from three separate systems, merges it algorithmically, and produces a median score that can look quite different from what any one bureau shows you.

The part that surprises people most is how a positive account missing from one bureau can quietly drag down their median score. A borrower might have a 760 on Experian, a 755 on Equifax, and a 718 on TransUnion because a key account never got reported to TransUnion. The lender uses 755, not 760. That gap costs nothing to fix if you catch it early and contact the creditor to request reporting to all three bureaus.

The single-bureau debate also concerns me for buyers entering the market now. A single-file framework may reduce costs but introduce uncertainty and increase long-term mortgage costs through risk premiums. If that shift happens, the buyers who understand how their data flows across bureaus will be far better positioned than those who do not. Checking mortgage rates and trends alongside your credit picture gives you the full context you need.

My honest advice: treat your credit reports as a living document, not a one-time check. The buyers who get the best rates are the ones who have been managing all three bureau files deliberately for at least six months before they walk into a lender’s office.

— Riley

How Rileychase helps you prepare for mortgage approval

Rileychase is built around one idea: you should understand exactly where you stand before you apply for a home loan. That starts with a thorough review of your credit picture across all three bureaus, not just a surface-level score check.

When you work with Rileychase on mortgage pre-approval, the process includes a full analysis of your tri-merge credit report, a clear explanation of how your scores affect your loan options, and a personalized plan for improving your position if needed. Whether you are looking at a fixed-rate conventional loan, an FHA product, or a VA loan, Rileychase walks you through how your credit data shapes each option. You deserve to go into the homebuying process with confidence, not guesswork about what a lender will find.

FAQ

What does a credit bureau do in the mortgage process?

A credit bureau collects and maintains records of your borrowing history and provides that data to lenders through a tri-merge credit report used for mortgage underwriting. Lenders use this data to assess your risk level and set your interest rate.

Why do lenders use all three credit bureaus for mortgages?

Lenders use all three bureaus because creditors are not required to report to every bureau, meaning each bureau may hold different data. The tri-merge report combines all three to reduce the risk of missing debts or errors that could distort the risk assessment.

What credit score does a lender use from a tri-merge report?

The lender uses the median, or middle, of your three bureau scores. If your scores are 700, 720, and 745, the qualifying score is 720.

How much can a score difference between bureaus affect my mortgage?

A score difference of 10 or more points between bureaus affects 35% of consumers and can shift a borrower into a different pricing tier. On a $350,000 loan, that shift can change total mortgage and insurance costs by $3,000 to $5,000.

How often should I check my credit reports before applying for a mortgage?

Pull all three bureau reports at least 90 days before applying. That timeline gives you enough time to dispute errors and see measurable improvement from any changes you make to your credit behavior.

Recommended

Related Posts