Discover the first-time buyer closing cost breakdown. Learn essential costs and budget effectively for your home purchase today!

The Role of a Title Company in Mortgage Closing

A title company is defined as a neutral third party that verifies property ownership, prepares closing documents, manages escrow funds, and issues title insurance during the mortgage closing process. The role of a title company in mortgage closing is far broader than most buyers realize. You sign dozens of documents, hand over tens of thousands of dollars, and walk away with keys. The title company makes sure every step of that transaction is legally sound and financially protected. Rileychase works with buyers at every stage of home financing, and understanding what a title company does helps you arrive at closing confident and prepared.

How does a title company conduct title searches and why are they essential?

A title search is the foundation of every real estate closing. Before any documents are signed or funds change hands, the title company combs through public records to confirm the seller has the legal right to sell the property. Title searches examine records spanning the past 20–50 years, covering court filings, tax databases, and deed histories. That depth of research exists because ownership problems from decades ago can still block a sale today.

The search uncovers issues that would surprise most buyers. Common problems include:

- Unpaid liens from contractors, lenders, or government agencies attached to the property

- Judgments against a previous owner that transferred with the title

- Easements granting third parties legal access to part of the land

- Ownership disputes from contested estates or missing heirs

- Recording errors where past deeds were filed incorrectly

Each of these defects can delay or kill a closing if left unresolved. The title company identifies them early and works with sellers, attorneys, and lienholders to clear them before the closing date. Standard title searches complete in 1–3 business days for most properties, though rural or historically complex properties can take longer. That timeline directly affects when your closing can be scheduled.

Pro Tip: Ask your title company for a copy of the preliminary title report as soon as it is available. Reviewing it early gives you time to ask questions and understand any issues before closing day.

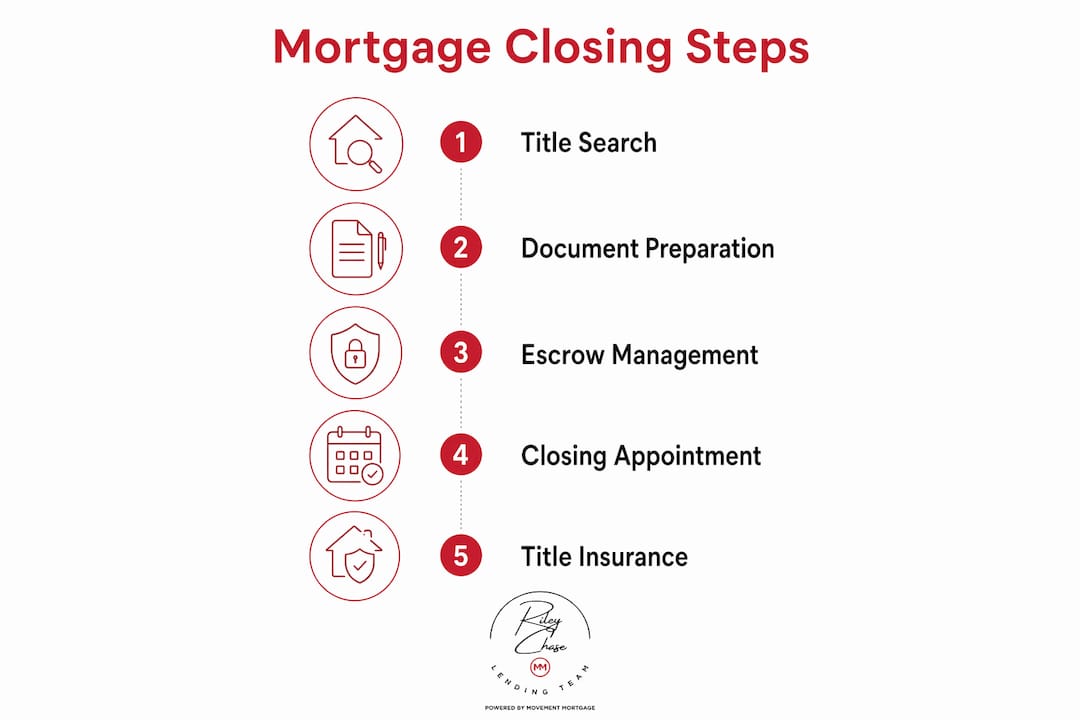

What happens during the mortgage closing appointment?

The closing appointment is where ownership officially transfers from seller to buyer. The title company’s closing agent runs the meeting, explains each document, and collects signatures. Knowing what to expect removes the stress from what is otherwise a fast-moving, paperwork-heavy event.

Here is what happens in order:

- Identity verification. You must bring two forms of valid government-issued identification. The title company confirms your identity before any documents are executed.

- Document review. The closing agent walks you through the Closing Disclosure, the promissory note, the deed of trust, and other loan documents. You have the right to read every page.

- Signing. You sign the mortgage and deed documents that transfer ownership and establish your loan obligations. The seller signs the deed over to you.

- Fund collection. You submit your down payment and closing costs via cashier’s check or wire transfer. Personal checks are never accepted at closing.

- Disbursement. The title company releases funds to the seller, real estate agents, and any lienholders once all conditions are satisfied.

- Recording. The title company sends the deed and mortgage to the county recorder’s office, making your ownership a matter of public record.

Closing appointments generally last between 1 and 2 hours. That window can shrink or expand depending on how prepared you are and whether any last-minute issues arise. You can learn more about what to expect on closing day to walk in fully prepared.

Pro Tip: Have your certified funds ready at least 1–2 days before closing. Wire transfers can take time to process, and any delay in funds will push your closing back.

How does the title company coordinate with lenders and manage escrow funds?

The title company acts as the operational hub between you, your lender, the seller, and every other party involved in the transaction. This coordination role is one of the most underappreciated parts of the mortgage closing process. Title companies act as the operational hub during closing, managing last-minute logistics for all parties beyond just paperwork.

The coordination responsibilities include:

- Receiving lender instructions. Your lender sends a detailed closing package with exact loan terms, funding conditions, and required signatures. The title company follows these instructions precisely.

- Preparing the settlement statement. The title company calculates prorations for property taxes and HOA fees, then prepares the Closing Disclosure that itemizes every dollar changing hands.

- Holding escrow funds. Earnest money, option fees, and your down payment sit in a dedicated escrow account. The title company holds all funds impartially until every closing condition is met.

- Disbursing payments. Once conditions are satisfied, the title company pays the seller, real estate agents, and any lienholders from the escrow account.

- Maintaining fiduciary duty. Escrow agents follow written instructions precisely, acting as neutral fiduciaries who cannot release funds early or take sides.

The fiduciary standard is what makes the title company trustworthy to all parties. Neither the buyer nor the seller can pressure the title company to release funds before the contract conditions are met. That neutrality protects you.

| Responsibility | Who benefits |

|---|---|

| Holding earnest money in escrow | Buyer and seller |

| Following lender closing instructions | Lender and buyer |

| Preparing the Closing Disclosure | All parties |

| Disbursing funds to seller and agents | Seller and agents |

| Recording the deed | Buyer |

Understanding closing costs in advance helps you verify the Closing Disclosure is accurate before you sign anything.

What is title insurance, and how does it protect you after closing?

Title insurance is a one-time policy that protects you from ownership problems discovered after you purchase the home. The title search catches most issues, but not every defect is visible in public records. Forged documents, undisclosed heirs, and recording errors can surface years after closing. Title insurance covers those risks.

There are two types of policies issued at closing:

- Lender’s title insurance. Required by virtually every mortgage lender. It protects the lender’s financial interest in the property up to the loan amount.

- Owner’s title insurance. Protects your equity and ownership rights. It is optional in most states but strongly recommended.

Title insurance covers risks including hidden claims, forged documents, undisclosed heirs, and recording errors that the title search did not catch. You pay a single premium at closing, and the coverage lasts as long as you own the home. Title insurance provides permanent coverage protecting homeowners from ownership disputes discovered after closing.

Store your title insurance policy in a safe place after closing. If a claim arises years later, you will need the policy number and coverage details to file. Storing the policy safely is one of the most practical steps you can take to protect your investment long term.

Key Takeaways

The title company is the neutral operational center of every mortgage closing, responsible for verifying ownership, managing funds, preparing documents, and issuing title insurance that protects buyers permanently.

| Point | Details |

|---|---|

| Title search scope | Searches cover 20–50 years of records to identify liens, judgments, and ownership disputes. |

| Closing day preparation | Bring two valid IDs, proof of homeowners insurance, and certified funds. Personal checks are rejected. |

| Escrow neutrality | The title company holds all funds impartially and disburses only when every closing condition is met. |

| Title insurance coverage | A one-time premium at closing provides permanent protection against hidden defects found after purchase. |

| Regional variation | Some states require a real estate attorney at closing; others let the title company manage the entire settlement. |

What I’ve learned about title companies that most buyers miss

Most buyers treat the title company as a formality. They show up, sign where they are told, and assume everything is handled. That mindset creates unnecessary risk.

The detail I see buyers overlook most often is the regional variation in title company authority. In some states, the title company manages nearly all settlement logistics. In others, a real estate attorney supervises or conducts the closing. If you are buying in an attorney-state and expect the title company to give you legal advice, you will be disappointed. The title company is a neutral fiduciary, not your legal counsel.

The second thing buyers miss is the importance of lender-title company communication. Delays at closing almost always trace back to a breakdown between the lender and the title company. A lender who sends closing instructions late, or a title company that does not flag a missing document quickly, can push your closing date back by days. Ask your lender early in the process which title company they work with regularly. A familiar working relationship between those two parties is worth more than you might think.

Finally, read your preliminary title report before closing day. Most buyers never ask for it. The report shows you exactly what the title company found and what issues, if any, are being resolved. That single step gives you real visibility into the health of the transaction.

— Riley

Rileychase is here to help you close with confidence

Reaching the closing table is a major milestone, and knowing how each piece fits together makes the experience far less stressful. Rileychase is built around helping buyers like you understand every step of the mortgage process, from your first loan question to the moment you get your keys.

Getting pre-approved for a mortgage before you shop gives you a clear budget and puts you in a stronger position when the title company prepares your closing documents. Rileychase also offers guidance on popular home loan types so you can choose the mortgage that fits your financial goals before you ever sit down at the closing table. When you are ready to take the next step, Rileychase is ready to walk through it with you.

FAQ

What does a title company do at mortgage closing?

A title company verifies property ownership, prepares closing documents, holds funds in escrow, coordinates with the lender, and issues title insurance. It acts as the neutral third party that ensures the transaction closes legally and securely.

How long does a title search take?

Most title searches complete in 1–3 business days. Properties with complex ownership histories or rural locations can take longer, which may affect your closing timeline.

Is title insurance required when buying a home?

Lender’s title insurance is required by nearly every mortgage lender. Owner’s title insurance is optional in most states but protects your equity against hidden defects discovered after closing.

What should I bring to my closing appointment?

Bring two forms of valid government-issued identification, proof of homeowners insurance, and certified funds in the form of a cashier’s check or wire transfer confirmation. Personal checks are not accepted.

Does the title company give legal advice at closing?

The title company does not provide legal advice. It is a neutral fiduciary that follows written instructions from the lender and the purchase contract. In some states, a real estate attorney is required to be present and can answer legal questions.

Recommended

Related Posts