Discover essential questions to ask mortgage lenders. Secure the best rates and avoid costly surprises by comparing offers effectively.

Why Mortgage Jargon Confuses Borrowers: 2026 Guide

Mortgage jargon is the specialized language of home financing, and its complexity is the leading cause of confusion among borrowers at every stage of the loan process. 58% of homeowners do not fully understand key home loan terms. That number means the majority of people signing one of the largest financial commitments of their lives are doing so without a clear picture of what they agreed to. Terms like Loan-to-Value ratio (LTV), Private Mortgage Insurance (PMI), debt-to-income ratio (DTI), and escrow appear all at once, with little context and even less explanation. Understanding why this happens is the first step toward fixing it.

Why mortgage jargon confuses borrowers

Mortgage terminology confusion does not happen by accident. The home loan industry uses a vocabulary built over decades by lawyers, underwriters, and regulators. That vocabulary was never designed with first-time buyers in mind.

Three forces drive the confusion:

- Technical complexity. Terms like LTV, DTI, and PMI each carry precise definitions that interact with each other. LTV affects whether you pay PMI. DTI determines your loan eligibility. Changing one number changes the others. Most borrowers encounter all three terms on the same day, with no explanation of how they connect.

- Inconsistent definitions across sources. A blog post, a lender’s website, and a mortgage broker may each describe an “offset account” differently. That inconsistency makes it hard to build a reliable mental model of how any single term works.

- The volume problem. Encountering multiple unfamiliar terms simultaneously causes borrowers to disengage from the process entirely. When everything is new at once, the brain defaults to shutting down rather than absorbing more.

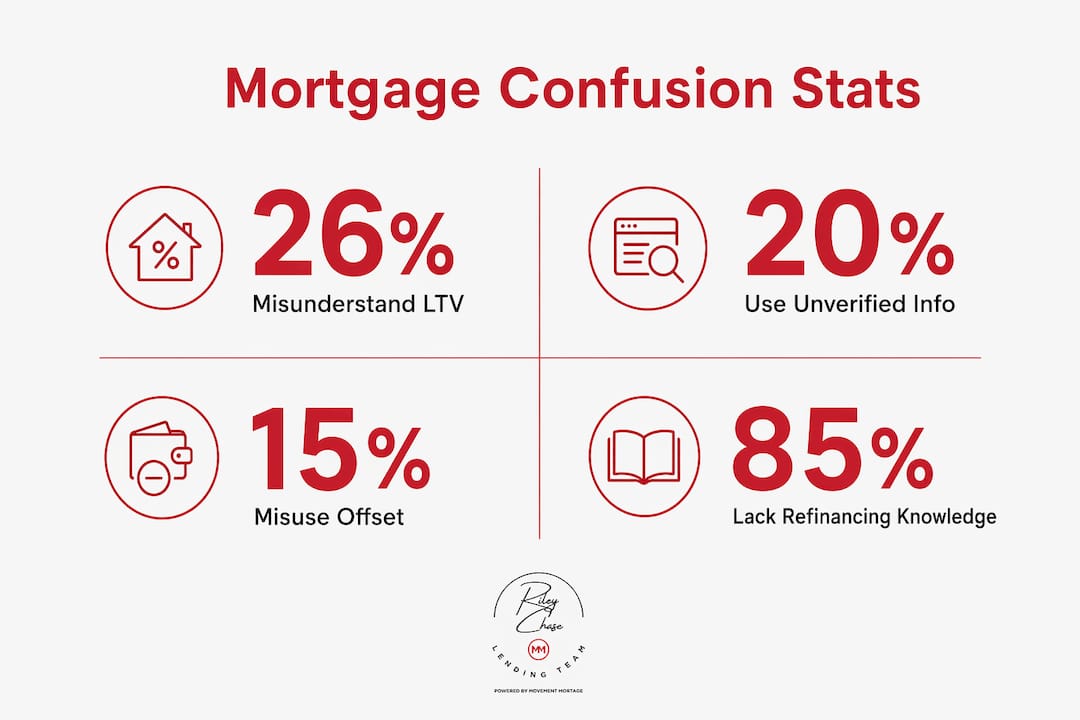

A fourth factor has grown significantly in 2026: misinformation from unverified sources. One in five borrowers rely on unverified AI tools for financial guidance. Social media compounds this by delivering oversimplified summaries that omit the details that actually matter.

Pro Tip: Before you trust any mortgage explanation you find online, check whether the source is a licensed lender, a regulated financial body, or a credentialed mortgage professional. If it is not, treat it as a starting point, not a final answer.

Which common mortgage terms do borrowers misunderstand the most?

Certain terms appear at the top of every confusion survey, and for good reason. Each one carries financial consequences when misunderstood.

| Term | What it means | Why borrowers get it wrong |

|---|---|---|

| LTV (Loan-to-Value ratio) | Your loan amount divided by the home’s appraised value | LTV is the most confusing term at 26%, often confused with down payment percentage |

| PMI / LMI | Insurance protecting the lender, not the borrower, when LTV exceeds 80% | Borrowers assume it protects them; 16% misunderstand when it applies |

| Offset account vs. redraw facility | Offset reduces interest daily; redraw lets you access extra repayments | Confused by 17% of borrowers; misuse leads to higher interest costs |

| Comparison rate | The true cost of a loan including fees, not just the advertised rate | 27% find hidden fees the most confusing part of home buying |

| Home equity | The portion of your home you actually own, not the full market value | 32% believe equity products are only for emergencies |

The LTV confusion carries the heaviest financial weight. If you do not understand your LTV ratio, you may not realize you are about to trigger a PMI requirement. That single misunderstanding can add hundreds of dollars to your monthly payment.

The offset account versus redraw distinction is equally costly. An offset account sits alongside your loan and reduces the balance on which interest is calculated, every single day. A redraw facility lets you pull back extra repayments you have already made. They sound similar. They work very differently. Borrowers who treat a redraw facility like an offset account often pay more interest than they need to.

Home equity misconceptions carry a different kind of cost. Viewing home equity as only an emergency tool limits your ability to use it for financial planning, debt consolidation, or investment. Experts treat equity as a planning asset, not a safety net. You can explore common mortgage myths that reinforce these kinds of misunderstandings.

How does misunderstanding mortgage jargon affect your decisions?

Confusion about mortgage language is not just frustrating. It costs money and leads to decisions that are hard to reverse.

“The mortgage industry has traditionally presented products as transactions rather than financial planning tools. That framing leaves borrowers without the context they need to make good decisions. When borrowers do not understand what they are buying, they cannot compare products, negotiate terms, or recognize when they are overpaying.”

The most direct cost shows up in PMI payments. A borrower who does not understand LTV may put down less than 20% without realizing they will pay PMI for years. That same borrower, with a clear explanation of how LTV and PMI connect, might choose to save longer or structure the purchase differently.

Misuse of offset accounts creates a quieter but equally real cost. A borrower who keeps savings in a standard account instead of an offset account pays interest on a higher loan balance every month. Over a 30-year loan, that difference compounds into a significant sum.

Pro Tip: Ask your lender or broker to show you the dollar impact of each term, not just the definition. “Your LTV is 85%” means less than “Because your LTV is 85%, you will pay $X per month in PMI until your balance drops below 80%.”

Confusion also creates a barrier to mortgage refinancing. Borrowers who do not understand their current loan terms cannot accurately evaluate whether a new loan is better. They either stay in a product that no longer fits their needs, or they refinance without understanding the true cost of switching. Both outcomes are preventable with better education upfront.

Confirmation bias makes this worse. Borrowers who find a simple explanation online tend to stop searching. They trust the first answer that sounds reasonable, even when it omits critical details. That pattern is especially common with AI-generated summaries, which often present accurate top-level definitions while missing the nuances that determine real-world outcomes.

What strategies actually help borrowers cut through the confusion?

Simplifying mortgage terminology requires a deliberate approach, from both borrowers and the professionals who guide them.

-

Learn terms in the order they appear in your loan process. Breaking mortgage concepts down chronologically reduces confusion and improves engagement. Start with pre-approval terms like DTI and credit score. Move to property-related terms like LTV and appraisal. Then address closing terms like escrow and origination fees. This sequence mirrors how the process actually unfolds.

-

Follow the related-term trail. Understanding how connected terms interact is more valuable than memorizing isolated definitions. LTV connects to PMI. PMI connects to your monthly payment. Your monthly payment connects to your DTI. Learning these relationships helps you see the full picture instead of a collection of disconnected acronyms.

-

Demand plain-language explanations from your lender or broker. A good mortgage professional explains what each term means for your specific loan, not just in general. If an explanation does not include a dollar amount or a percentage that applies to your situation, ask for one.

-

Avoid unverified AI and social media advice as your primary source. Use these tools to generate questions, not answers. Then bring those questions to a licensed professional who can give you context-specific guidance.

-

Use structured educational resources. Rileychase’s mortgage terms guide for first-time buyers walks through key vocabulary in plain language, connected to the stages of the loan process where each term matters.

The lender’s role matters here too. Lenders who understand borrower goals before recommending products give borrowers a much clearer framework for understanding terminology. A term like “home equity line of credit” makes more sense when it is presented as a tool for a specific goal, not as a product feature on a rate sheet.

Key Takeaways

Mortgage terminology confusion is preventable when borrowers learn terms in sequence, understand how concepts connect, and work with professionals who explain the real-dollar impact of each term.

| Point | Details |

|---|---|

| LTV is the most misunderstood term | 26% of borrowers confuse LTV, which directly triggers PMI costs when it exceeds 80%. |

| Offset accounts and redraw facilities differ significantly | Misusing these features leads to higher interest payments over the life of the loan. |

| Hidden fees confuse 27% of borrowers | Always request a comparison rate, not just the advertised interest rate. |

| Unverified AI advice increases financial risk | One in five borrowers rely on unverified AI tools; use them to form questions, not conclusions. |

| Sequential learning reduces confusion | Learning terms in the order they appear in the loan process improves comprehension and engagement. |

What I’ve learned from watching borrowers navigate mortgage confusion

Working with borrowers across every experience level, I have noticed one consistent pattern: the borrowers who struggle most are not the ones who ask too many questions. They are the ones who stop asking because they feel embarrassed by what they do not know.

Mortgage language was not designed to be accessible. It evolved inside an industry that prioritized precision over clarity. That is not an excuse. It is a problem worth solving, and the solution starts with borrowers feeling confident enough to say, “I do not understand that. Can you explain it differently?”

The rise of AI-generated mortgage advice worries me more than any other trend I have seen. A borrower who reads a clean, confident AI summary about offset accounts may walk away thinking they understand the concept, when in reality they have only absorbed the surface-level definition. The details that determine whether an offset account saves them money or costs them money are exactly the kind of nuance that gets stripped out in a summary.

My honest recommendation: treat every online explanation as a starting point. Then bring your questions to a professional who can connect the definition to your actual loan numbers. The goal is not to memorize terminology. The goal is to understand what each term means for your monthly payment, your total interest cost, and your long-term financial position. That understanding is worth more than any glossary.

— Riley

Rileychase makes mortgage terminology work for you

Mortgage language should not stand between you and the home you want. Rileychase works with first-time buyers and experienced homeowners to explain every term in plain language, connected to your specific loan situation.

Whether you are trying to understand the difference between a fixed-rate and an adjustable-rate loan, or you want to know exactly how your LTV affects your monthly payment, Rileychase’s team walks you through it step by step. The pre-approval process is the best place to start. It gives you a clear picture of your budget and surfaces the terms that matter most for your situation before you ever make an offer. You can also review your loan options to see how different products compare in plain terms.

FAQ

What is the most confusing mortgage term for borrowers?

LTV, or Loan-to-Value ratio, is the most confusing mortgage term, with 26% of borrowers reporting they do not understand it. Misunderstanding LTV often leads to unexpected PMI costs.

Why does mortgage jargon cause so many borrowers to disengage?

Encountering multiple unfamiliar terms at once causes borrowers to disengage from the loan process entirely. Lenders who introduce terms sequentially, in the order they appear in the process, see significantly better borrower engagement.

Is it safe to use AI tools to learn mortgage terms?

AI tools can help you generate questions, but one in five borrowers who rely on them for financial guidance risk acting on incomplete or misleading information. Always verify AI-generated explanations with a licensed mortgage professional.

What is the difference between an offset account and a redraw facility?

An offset account reduces the loan balance on which interest is calculated daily, while a redraw facility lets you access extra repayments you have already made. Using the wrong one for your goals can result in paying more interest over the life of your loan.

How can I avoid being misled by hidden mortgage fees?

Always ask for the comparison rate, not just the advertised interest rate. The comparison rate includes fees and charges, giving you a more accurate picture of the loan’s true cost.

Recommended

Related Posts