Explore refinance underwater mortgage options in 2026. Understand your choices for FHA, VA, and USDA loans to regain financial control.

Why Mortgage Fees Vary by Lender: 2026 Guide

Mortgage fees vary by lender because each lender sets its own origination charges, builds in different rate-fee trade-offs, and operates under a unique business model that shapes every line on your Loan Estimate. The industry term for these upfront costs is “closing costs,” and the lender-controlled portion, called origination fees, typically ranges from 0.5% to 1.0% of the loan amount. On a $350,000 mortgage, that gap alone equals $1,750 to $3,500 before you factor in other lender charges. Understanding why mortgage fees vary by lender is the first step toward saving thousands on your home purchase.

Why mortgage fees vary by lender: origination charges explained

Origination fees are the primary reason lender fee comparison reveals such wide cost differences. These charges compensate the lender for processing, underwriting, and funding your loan. They are not standardized across the industry, which means every lender prices them based on its own cost structure and profit targets.

Total loan costs among major lenders range from as low as $4,856 to over $9,200 for the same type of purchase mortgage. That spread of more than $4,300 exists before you even add prepaid items like homeowners insurance or property taxes. The gap is real, and it is entirely within your control to close it by shopping around.

Several factors drive origination fee differences from one lender to the next:

- Overhead costs. Lenders with large branch networks and dedicated loan officers carry higher operating expenses, which get passed to borrowers through fees.

- Loan officer compensation. Commission structures tied to loan amounts create incentives that directly affect what you pay. Loan officers may reduce or waive fees when presented with a competing Loan Estimate.

- Volume and efficiency. High-volume lenders that process thousands of loans monthly often spread fixed costs across more transactions, allowing lower per-loan fees.

- Fee waivers as sales tools. Some lenders waive processing or underwriting fees to win your business, then recover the cost through a slightly higher interest rate.

Pro Tip: Ask every lender to itemize origination charges separately from third-party fees. A single “origination fee” line can bundle multiple charges, making it harder to compare lenders accurately.

How do lenders balance interest rates and fees?

The rate-fee trade-off is one of the most misunderstood factors affecting mortgage fees. Lenders adjust upfront fees and interest rates together to create different cost structures that all appear competitive on the surface.

Here is how the trade-off works in practice:

- Lower rate, higher fees. A lender offers 6.25% with $4,000 in origination fees. You pay more upfront but less each month.

- Higher rate, lower fees. A different lender offers 6.625% with $1,500 in origination fees. Your monthly payment is higher, but you bring less cash to closing.

- Discount points. Paying one discount point (1% of the loan amount) typically buys down the rate by a set amount. On a $350,000 loan, one point costs $3,500.

- No-cost loans. Some lenders advertise zero origination fees but price the rate higher to recoup costs over time.

Lenders balance rates and fees strategically, which means a low advertised rate does not equal a low-cost loan. The Annual Percentage Rate (APR) on your Loan Estimate combines the interest rate and fees into a single number, making it a far better comparison tool than the rate alone.

“Evaluating APR instead of the advertised interest rate provides better insight into the true cost of the mortgage when fees and rate trade-offs are factored in.”

Your expected time in the home matters here. If you plan to sell or refinance within five years, paying discount points rarely makes financial sense. Borrowers holding a home longer may benefit from paying points upfront, but always calculate the break-even timeline before committing.

Which mortgage fees are negotiable?

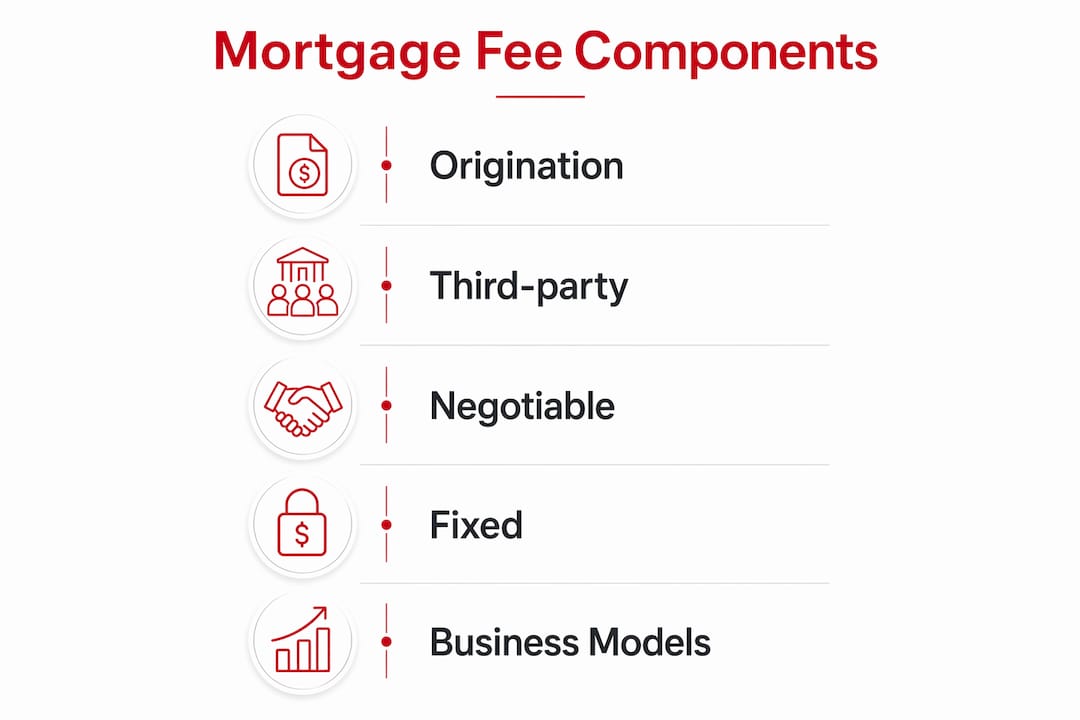

Not all fees on your Loan Estimate are equal. The Consumer Financial Protection Bureau (CFPB) structures the Loan Estimate into sections that tell you exactly where lender flexibility exists.

Section A: Origination charges. These are 100% lender-controlled. Origination fees, underwriting fees, processing fees, and application fees all live here. These are the most negotiable items on the entire document.

Section B: Services you cannot shop for. This includes the appraisal, credit report, and flood determination. Third-party fees like appraisals and title insurance are generally non-negotiable because lenders have little control over vendor pricing or local regulations.

Section C: Services you can shop for. Title search, title insurance, and settlement services fall here. You can choose your own vendors for these, which gives you a real opportunity to reduce costs.

Watch for “junk fees” in Section A. These include charges with vague names like “administrative fee,” “document preparation fee,” or “courier fee.” They add cost without adding value and are almost always negotiable or removable entirely.

Pro Tip: Print out Loan Estimates from at least three lenders and lay them side by side. Focus your negotiation on Section A charges. Show a lender a lower competing estimate and ask them to match or beat it.

How do lender business models affect your fees?

A lender’s business model directly shapes its fee structure, and understanding this helps you know what to expect before you apply.

- Retail lenders with branch networks. These lenders offer in-person support and dedicated loan officers. Their higher overhead typically produces higher origination fees, but the personalized guidance can be worth it for first-time buyers.

- Direct and automated lenders. Online-focused platforms with less human involvement often charge lower fees because their cost per loan is lower. The trade-off is less hands-on support during the process.

- Mortgage brokers. Brokers shop your application across multiple wholesale lenders. They can find competitive rates and fees, but their compensation (paid by the lender or the borrower) adds a layer to the cost structure.

- Builder in-house lenders. When you buy a new construction home, the builder’s preferred lender may offer closing cost credits as an incentive. These credits can offset fees, but the underlying rate may be less competitive.

Lenders that originate more FHA or jumbo loans carry different fee profiles than those focused on conventional loans. A lender specializing in FHA loans may show higher average fees in industry data simply because FHA loans require additional compliance steps. Comparing lenders within the same loan type gives you a cleaner picture of true variability in mortgage costs.

How can homebuyers compare mortgage fees effectively?

The CFPB recommends requesting Loan Estimates from at least three lenders simultaneously. Doing this within a short window limits the impact on your credit score, since multiple mortgage inquiries within 45 days typically count as a single inquiry under FICO scoring models.

Follow these steps to compare Loan Estimates with confidence:

- Request estimates on the same day. Rates change daily. Getting all estimates on the same day makes the comparison valid.

- Go straight to Section A. Origination charges are where lender fee differences are largest and most negotiable. Compare this section first.

- Compare APR, not just rate. The APR reflects the combined cost of the rate and fees. A lower APR means a lower total cost, assuming you hold the loan to term.

- Check “cash to close.” This number on page 2 of the Loan Estimate shows exactly what you need to bring to the closing table. It is the most practical single-number comparison.

- Use estimates as leverage. Bring a lower competing estimate to your preferred lender and ask them to match it. Origination and processing fees are the most commonly adjusted items when borrowers negotiate.

Understanding closing costs in full detail before you apply puts you in a much stronger negotiating position. Borrowers who arrive prepared consistently secure better terms than those who accept the first offer.

Key Takeaways

Mortgage fees vary by lender primarily because origination charges, rate-fee trade-offs, and lender business models create structural cost differences that borrowers can identify, compare, and negotiate using standardized Loan Estimates.

| Point | Details |

|---|---|

| Origination fees drive the biggest gap | Fees range from 0.5% to 1.0% of the loan, creating a $1,750–$3,500 spread on a $350,000 mortgage. |

| APR beats rate as a comparison tool | APR combines the interest rate and fees, giving you a single accurate measure of total loan cost. |

| Section A fees are negotiable | Origination, underwriting, and processing fees are lender-controlled and can be reduced with competing quotes. |

| Business model shapes fee structure | Retail lenders, direct lenders, brokers, and builder lenders each carry different cost structures and fee levels. |

| Shop at least three lenders | Requesting multiple Loan Estimates within 45 days protects your credit score while maximizing your negotiating leverage. |

What I’ve learned after years of watching borrowers leave money on the table

Most borrowers focus entirely on the interest rate and barely glance at the fee columns. That is the single most expensive mistake you can make in the mortgage process.

I have seen borrowers choose a lender with a rate that was 0.125% lower, only to pay $3,000 more in origination fees. The math did not work in their favor, especially since they sold the home four years later. The lower-rate lender cost them money. This is why I always say: the rate is the headline, but the fees are the story.

The other thing most articles skip is how willing lenders actually are to negotiate. Loan officers work on commission. They want your loan. Showing up with a competing Loan Estimate is not aggressive or awkward. It is expected. I have watched borrowers get $1,500 in fees removed in a single phone call simply by saying, “Another lender is offering me this. Can you match it?” That conversation takes five minutes and can save you real money.

One more thing: your timeline matters more than most people realize. If you are buying your forever home, paying a point upfront to lock in a lower rate makes sense. If you are buying a starter home you plan to sell in three to five years, paying points is almost always a losing trade. Know your timeline before you decide between a lower rate with higher fees or a higher rate with lower fees.

The mortgage approval process rewards preparation. Borrowers who understand fee structures before they apply negotiate from a position of knowledge, not anxiety.

— Riley

How Rileychase helps you prepare for mortgage costs

Knowing why mortgage costs vary is powerful. Knowing how to prepare your finances before you apply is what turns that knowledge into savings.

Rileychase offers clear, practical resources built for homebuyers at every stage. Whether you are comparing common mortgage types to understand which loan fits your situation, or working through the steps to prepare financially for homeownership, Rileychase guides you through the process with transparency and real support. You will find tools to strengthen your application, understand your budget, and walk into lender conversations with confidence. Start with the financial preparation guide and see exactly where you stand before you request your first Loan Estimate.

FAQ

What is a mortgage origination fee?

A mortgage origination fee is the charge a lender applies to cover the cost of processing and underwriting your loan. It typically ranges from 0.5% to 1.0% of the loan amount and is the most negotiable fee on your Loan Estimate.

Why do mortgage fees differ so much between lenders?

Mortgage fee differences come from each lender’s overhead costs, loan officer compensation models, business structure, and rate-fee trade-off decisions. Median total loan costs among major lenders vary by more than $4,300 for the same type of purchase mortgage.

Can I negotiate mortgage fees with my lender?

Yes. Origination, underwriting, and processing fees in Section A of the Loan Estimate are negotiable. Presenting a competing Loan Estimate gives you direct leverage, and loan officers frequently adjust fees to retain borrowers.

What is the best way to compare mortgage fees across lenders?

Request Loan Estimates from at least three lenders on the same day, then compare Section A charges and the APR. The CFPB recommends this approach as the most reliable method for an apples-to-apples fee comparison.

Are all closing costs set by the lender?

No. Third-party fees such as appraisals, title insurance, and credit reports are largely fixed by vendors and local regulations. Only lender-controlled fees in Section A of the Loan Estimate are negotiable.

Recommended

Related Posts