Discover why mortgage fees vary by lender and learn how to save thousands on your home purchase with our 2026 guide.

Refinance Underwater Mortgage Options: 2026 Guide

An underwater mortgage is defined as a home loan where you owe more than your property is currently worth. Refinancing an underwater mortgage is possible, but your options depend almost entirely on your loan type. Homeowners with FHA, VA, or USDA loans can access government-backed streamline refinance programs that skip the appraisal entirely. Conventional loan holders face a narrower path, relying on cash-in refinancing or loan modifications. This guide breaks down every realistic option for underwater mortgage solutions in 2026, so you can move forward with confidence rather than confusion.

What are the refinance underwater mortgage options by loan type?

The most direct path to refinancing an underwater home depends on whether your loan is government-backed or conventional. Government-backed streamline programs waive appraisal requirements and allow refinancing regardless of negative equity, which is the single biggest advantage they offer. That means your home’s current market value does not block your application.

Three programs cover the majority of eligible homeowners:

- FHA Streamline Refinance: Available to homeowners with existing FHA loans. You must be current on payments and show a net tangible benefit, such as a lower monthly payment or a move from an adjustable to a fixed rate. No income verification or appraisal is required in most cases.

- VA Interest Rate Reduction Refinance Loan (IRRRL): Designed for veterans and active-duty service members with existing VA loans. The VA IRRRL reduces your interest rate with minimal paperwork. You do not need a new appraisal or credit underwriting in most scenarios. Learn more about VA vs. conventional loans to confirm your eligibility.

- USDA Streamlined Assist Refinance: For homeowners in rural areas with existing USDA loans. This program requires no appraisal, no credit review, and no debt-to-income calculation. Your payment must decrease by at least $50 per month to qualify.

All three programs share a critical feature: they do not require your home to appraise at or above your loan balance. That is what makes them the strongest mortgage refinancing options for underwater homeowners.

Pro Tip: Before applying for any streamline program, pull your original loan documents to confirm your loan type. Many homeowners assume they have a conventional loan when they actually have an FHA or USDA loan, which changes everything.

Eligibility for each program does require that you are current on your mortgage. A history of on-time payments, typically 12 months or more, strengthens your application significantly.

How can homeowners with conventional loans refinance underwater mortgages?

Conventional loan holders face a harder reality. No current government-backed streamline program exists for conventional underwater mortgages after the Home Affordable Refinance Program (HARP) expired. That program ended in 2018, and no direct replacement has been created for conventional loans. Your options are narrower, but they are not zero.

The primary path for conventional loan holders is a cash-in refinance. Here is how it works:

- Calculate your current loan-to-value ratio (LTV). Divide your remaining loan balance by your home’s current appraised value. If you owe $220,000 and your home is worth $200,000, your LTV is 110%.

- Determine how much cash you need to bring. Most lenders require an LTV between 95% and 97% to approve a conventional refinance. In the example above, you would need to reduce your balance to roughly $190,000 to $194,000, meaning you bring $26,000 to $30,000 to closing.

- Source and season your funds. Lenders require documented proof that your cash has been in your account for at least 60 days. Funds that appear suddenly or come from undocumented gifts raise red flags and cause denials.

- Apply with your current lender first. Your existing servicer may be more flexible than a new lender because they already hold the risk on your loan.

- Ask about portfolio lenders. Some smaller banks and credit unions hold loans on their own books rather than selling them to investors. Portfolio lenders may manually underwrite high-LTV loans, though their criteria are stricter and approval is not guaranteed.

| Option | LTV Requirement | Appraisal Needed | Cash Required |

|---|---|---|---|

| Cash-in refinance | 95%–97% | Yes | Yes |

| Portfolio lender refinance | Varies | Usually yes | Possibly |

| FHA/VA/USDA streamline | No limit | No | No |

Pro Tip: Document your cash-in funds carefully. “Sourced and seasoned” means your lender wants bank statements showing the money has been sitting in your account, not a wire transfer that arrived last week. Missing this step is one of the most common reasons cash-in refinances get denied.

Weigh the cost of bringing cash to closing against your long-term savings. If your new rate saves you $150 per month and you spend $25,000 to close, your break-even point is roughly 14 years. That math matters before you commit.

What are your options when refinancing an underwater mortgage isn’t feasible?

When refinancing is not possible, a loan modification is the next best tool. A loan modification adjusts the terms of your existing mortgage without replacing it. Loan modifications can reduce your interest rate, extend your loan term, or both, making your monthly payment more manageable without requiring a new appraisal or equity position.

To qualify, you typically need to demonstrate financial hardship. That means documenting reduced income, job loss, medical expenses, or another event that makes your current payment unaffordable. Your servicer reviews this documentation and decides whether to offer modified terms.

Key points to understand about modifications:

- They do not erase your negative equity. They make payments more affordable while you wait for your home value to recover.

- Short sales and loan modifications carry credit and tax consequences. Forgiven debt may count as taxable income. Consult a tax professional or a HUD-approved housing counselor before signing anything.

- A modification stays on your credit report and can affect your ability to borrow in the future.

Proactive communication with your servicer is the single most important step you can take. Waiting until you miss payments reduces the number of options available to you. Call before you fall behind.

If neither refinancing nor modification fits your situation, staying put is a legitimate strategy. Making extra principal payments gradually builds equity and positions you for a conventional refinance once your LTV improves. This approach avoids the credit damage that comes with a short sale or foreclosure, and it keeps your long-term financial health intact.

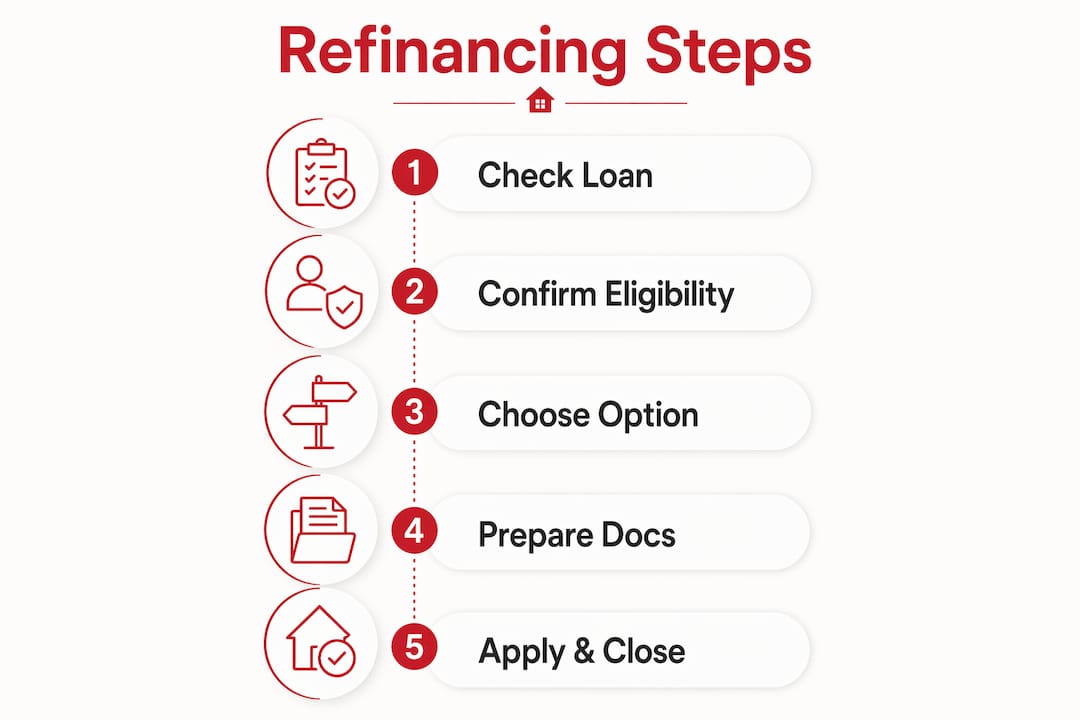

How do you prepare and apply for underwater mortgage help?

Preparation separates successful applications from rejected ones. Follow these steps before you contact any lender or servicer.

- Identify your loan type. Check your original closing documents or call your servicer. Confirm whether you have an FHA, VA, USDA, or conventional loan. This single fact determines which programs you can access.

- Calculate your LTV. Get a current estimate of your home’s value through a licensed appraiser or a real estate agent’s comparative market analysis. Divide your balance by that value to find your LTV.

- Check program eligibility. For streamline programs, confirm you are current on payments and have held the loan for the required minimum period, typically six to twelve months.

- Gather your documents. Collect recent pay stubs, two years of tax returns, two to three months of bank statements, and your most recent mortgage statement. For mortgage refinance preparation, having these ready before you apply speeds up the process considerably.

- Contact a HUD-approved counselor. Free counseling is available through the U.S. Department of Housing and Urban Development. Counselors help you evaluate your options without any sales pressure.

- Use a mortgage calculator. Run the numbers on your potential new payment before you apply. Knowing your break-even point helps you decide whether refinancing makes financial sense right now.

Pro Tip: Apply when your financial picture is at its strongest. If you are expecting a raise or a tax refund, timing your application to reflect higher income or lower debt can improve your approval odds significantly.

Avoid these common mistakes: applying with multiple lenders in a short window without understanding how credit inquiries work, submitting incomplete documentation, and accepting verbal assurances from servicers without getting terms in writing.

Key takeaways

Homeowners with FHA, VA, or USDA loans have the strongest refinancing options through government-backed streamline programs that require no appraisal, while conventional loan holders must rely on cash-in refinancing, portfolio lenders, or loan modifications.

| Point | Details |

|---|---|

| Loan type determines your options | FHA, VA, and USDA loans qualify for streamline refinances; conventional loans do not. |

| Streamline programs skip appraisals | Government-backed programs allow refinancing regardless of negative equity. |

| Cash-in refinance requires documentation | Funds must be sourced and seasoned for at least 60 days to satisfy lenders. |

| Loan modifications are a real alternative | Modifications adjust terms to reduce payments without requiring equity or refinancing. |

| Early communication matters | Contacting your servicer before missing payments preserves more options. |

What I’ve learned about underwater mortgages that most articles won’t tell you

The biggest misconception I see is that homeowners expect a broad federal rescue program to appear and fix everything. No universal federal bailout exists for underwater conventional mortgages. The relief that does exist is targeted, program-specific, and tied directly to your loan type. Expecting otherwise leads to wasted months and missed opportunities.

The homeowners who come out ahead are not the ones who wait for the market to save them. They are the ones who call their servicer early, get their documents in order, and make a decision based on real numbers rather than hope. I have seen homeowners with steady incomes make significant progress simply by paying down principal consistently over two to three years, then refinancing once their LTV crossed the threshold.

Credit impact is also underestimated. A short sale feels like relief in the moment, but it follows you for years. A modification is less damaging, but it still shows up. If you can stay current and work the problem methodically, your future self will thank you.

My honest advice: treat your loan type as the starting point, not your home value. Your home value is a market variable you cannot control. Your loan type is a fact that opens or closes specific doors. Know which door you are standing in front of, then work the options that actually exist for you.

— Riley

Rileychase can help you prepare for what comes next

Navigating underwater mortgage solutions takes more than good intentions. It takes financial preparation, the right documentation, and a clear understanding of which programs apply to your situation.

Rileychase provides the educational resources and personalized guidance you need to approach refinancing or modification with confidence. Whether you are working toward improving your approval chances or building the financial foundation to qualify for a streamline program, the team at Rileychase is ready to walk you through it. Start with the five-step financial preparation guide to get your finances in the best possible shape before you apply.

FAQ

What is an underwater mortgage?

An underwater mortgage is one where your remaining loan balance exceeds your home’s current market value, resulting in negative equity. This limits your ability to sell or refinance through traditional means.

Can I refinance if I have an FHA loan and negative equity?

Yes. The FHA Streamline Refinance allows you to refinance regardless of your home’s current value, with no appraisal required, as long as you are current on payments and demonstrate a net tangible benefit.

What happened to HARP for conventional loans?

The Home Affordable Refinance Program expired in 2018 and was not replaced with an equivalent program for conventional loans. Conventional loan holders must use cash-in refinancing or seek portfolio lenders instead.

How does a loan modification differ from a refinance?

A loan modification changes the terms of your existing loan without replacing it, typically by reducing the rate or extending the term. A refinance replaces your current loan with a new one, usually requiring equity or a cash contribution.

Will a loan modification hurt my credit?

A loan modification can appear on your credit report and may affect your score, but it is generally less damaging than a foreclosure or short sale. Consulting a HUD-approved counselor before agreeing to any modification terms is strongly recommended.

Recommended

Related Posts