Explore key loan types for competitive real estate markets in 2026. Make informed choices to boost your offer strength and close faster.

The Role of Down Payment Explained for Homebuyers

A down payment is the upfront cash you pay toward a home’s purchase price, and it directly reduces your loan principal, monthly payment, and total interest from day one. Understanding the role of down payment explained in full means knowing it does far more than shrink the loan balance. It shapes your interest rate, determines whether you pay private mortgage insurance (PMI), and signals your financial reliability to lenders. The standard industry term for this concept is “initial equity contribution,” though most buyers and lenders simply call it the down payment. Getting this number right is one of the most consequential decisions in the entire homebuying process.

How does the down payment role affect your mortgage costs?

A down payment affects four financial levers at once: loan size, PMI cost, interest rate pricing, and the cash you keep after closing. Most buyers focus only on the monthly payment, but the ripple effects go much further. Choosing the right amount requires you to weigh all four levers together, not just one.

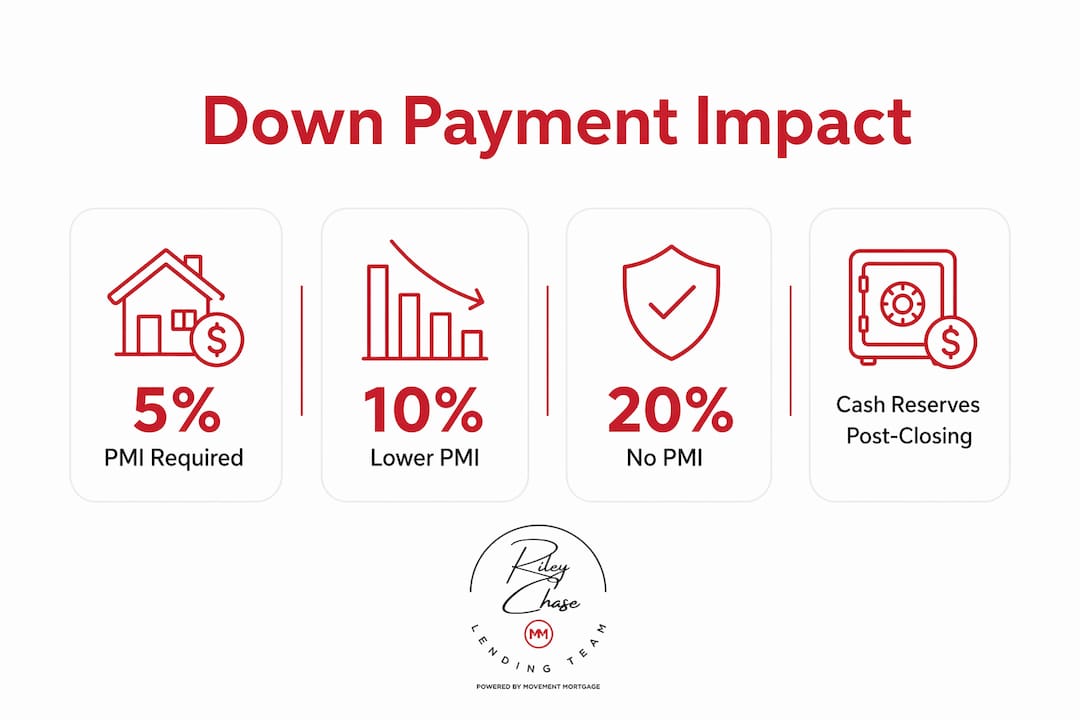

The 5%, 10%, and 20% breakdown

The three most common down payment thresholds each produce a distinct financial outcome.

- 5% down preserves your cash reserves but increases your loan balance and triggers PMI. Your monthly payment is higher, and you pay more interest over the life of the loan. This option works best when you have stable income but limited savings.

- 10% down is the middle ground. It balances payment size with liquidity and gives you a path to remove PMI later through home appreciation or extra principal payments. Many experienced buyers prefer this level precisely because it keeps cash available for post-closing costs.

- 20% down eliminates PMI entirely and often qualifies you for a lower interest rate. On a $400,000 loan, avoiding PMI saves $120–$280 monthly. Over a 30-year term, that adds up to tens of thousands of dollars.

| Down payment | PMI required | Monthly payment impact | Cash reserves after closing |

|---|---|---|---|

| 5% | Yes | Highest | Strong |

| 10% | Yes (removable) | Moderate | Moderate |

| 20% | No | Lowest | Reduced |

Pro Tip: Calculate your post-closing cash position before committing to a down payment amount. Closing costs, moving expenses, and first-year repairs can easily total $10,000 or more on a median-priced home.

Why do cash reserves matter when choosing a down payment amount?

Depleting your savings to reach a higher down payment target creates a financial vulnerability that most buyers underestimate. Homeownership carries significant first-year cash demands beyond the purchase itself, including repairs, furnishings, and unexpected maintenance. Stretching too far for a larger down payment can leave you exposed the moment something breaks.

The risks of low liquidity after closing are real and specific:

- Emergency repairs: A failed HVAC system or roof leak can cost $5,000–$15,000 with little warning.

- Income disruption: A job change or medical event hits much harder when your savings account is near zero.

- Missed opportunities: Low cash reserves prevent you from acting quickly on refinancing or home improvements that build equity.

Large down payments only make sense when your emergency fund stays intact after closing. Experts consistently recommend keeping three to six months of living expenses in reserve, separate from any funds used for the down payment. Treating those reserves as untouchable is not conservative thinking. It is sound financial planning.

Pro Tip: Before finalizing your down payment amount, list every expected first-year homeownership cost. Subtract that total from your available savings. The remainder is your true down payment ceiling.

How does a larger down payment improve mortgage approval chances?

A down payment reduces lender risk and signals borrower commitment, which directly influences your loan terms and approval likelihood. Lenders view a larger down payment as evidence that you manage money well and have skin in the game. That perception translates into real advantages during underwriting.

A stronger down payment position helps you in three concrete ways:

- Loan approval: Lenders are more willing to approve buyers who bring more equity upfront, especially if other factors like credit score or debt-to-income ratio are borderline.

- Interest rate pricing: A larger down payment can qualify you for a lower rate tier, reducing your cost over the entire loan term.

- Competitive offers: In a bidding war, a buyer with 20% down is often more attractive to a seller than one with 5% down, because the deal is less likely to fall apart during financing.

Larger down payments improve affordability in high borrowing cost environments and position buyers more competitively. Knowing how to improve your mortgage approval chances before you make an offer gives you a real edge. The down payment is one of the fastest levers you can pull to strengthen your application.

Can waiting to save more actually cost you more?

Delaying your purchase to save a larger down payment can backfire if home prices and interest rates rise in the meantime. The math on waiting is not always favorable, and buyers often underestimate how quickly market conditions can shift.

Consider this sequence:

- You decide to wait 18 months to save an additional $20,000 for a larger down payment.

- Home prices in your target market rise 6% during that period.

- The home you wanted at $400,000 now costs $424,000.

- Your larger down payment no longer covers the same percentage of the purchase price.

- Your monthly payment may be higher than it would have been if you had bought earlier with a smaller down payment.

Rising interest rates affect your homebuying power in a compounding way. A rate increase of even 0.5% on a $380,000 loan adds hundreds of dollars per month and tens of thousands over the loan term. Waiting is not inherently wrong, but it carries a real cost that buyers rarely calculate in advance.

Pro Tip: Run a side-by-side cost comparison: buying now with a smaller down payment versus buying in 12–18 months with a larger one. Factor in projected price appreciation and rate changes. The results often surprise buyers who assumed waiting was the safer choice.

How do you decide the right down payment amount for your situation?

The right down payment amount is the one that fits your financial picture, not a fixed percentage rule. Start by assessing your total available cash, then subtract your emergency fund, estimated closing costs, and first-year homeownership expenses. What remains is your realistic down payment range.

Use this framework to evaluate your options:

- Assess total liquidity: Add up all savings, investment accounts you can access, and gift funds. Do not count retirement accounts unless you understand the tax consequences.

- Calculate true affordability: Use a mortgage calculator to compare monthly payments at different down payment levels. Make sure the payment fits your budget with room to spare.

- Explore low down payment programs: FHA loans allow as little as 3.5% down for qualified buyers. VA loans require no down payment for eligible veterans. Low down payment purchase options exist for buyers who need to preserve liquidity.

- Align with your timeline: If you plan to sell within five years, a lower down payment may make more sense. If this is your long-term home, building equity faster has real value.

- Factor in PMI removal: A 10% down payment with a plan to remove PMI through appreciation is a legitimate strategy. Buyers can remove PMI later once they reach 20% equity, making the initial cost temporary.

A down payment is a strategic decision that balances short-term liquidity with long-term mortgage costs. No single percentage is universally correct. The best amount is the one that keeps you financially stable on day one and every month after.

Key Takeaways

A down payment directly controls your loan size, PMI obligation, interest rate, and post-closing cash reserves, making it the single most impactful financial decision in the homebuying process.

| Point | Details |

|---|---|

| Down payment reduces loan costs | A larger down payment lowers your principal, monthly payment, and total interest paid. |

| 20% down eliminates PMI | Avoiding PMI on a $400,000 loan saves $120–$280 per month. |

| Cash reserves must stay intact | Never deplete emergency savings for a larger down payment. |

| Waiting to save more can cost more | Rising home prices and rates can outpace the savings gained by delaying purchase. |

| Right amount is personal | Assess liquidity, timeline, and monthly affordability before choosing a down payment level. |

What I’ve learned about down payments after years of helping buyers

Most buyers come to me fixated on hitting 20% down. I understand the appeal. It is a clean number, it eliminates PMI, and it feels like the “responsible” choice. But I have watched buyers drain their savings to reach that threshold, close on their home, and then panic three months later when the water heater fails and they have nothing left to cover it.

The buyers who fare best are not the ones who put down the most. They are the ones who put down the right amount for their specific situation. I have seen buyers thrive with 10% down because they kept a healthy cash cushion and had a clear plan to remove PMI within two years through appreciation. I have also seen buyers struggle after putting 25% down because they had no buffer for the unexpected costs that every homeowner eventually faces.

Market conditions matter too. When rates are rising and prices are climbing, waiting to save more can genuinely cost you more in the long run. The calculation is not just about the down payment. It is about the total cost of the home over time, including the opportunity cost of waiting.

My honest advice: treat your emergency fund as non-negotiable. Build your down payment strategy around what is left. A slightly higher monthly payment is manageable. A financial emergency with no reserves is not.

— Riley

Rileychase can help you plan your down payment with confidence

Choosing the right down payment amount is easier when you have a clear picture of your full financial position and the loan options available to you.

Rileychase works with first-time buyers and experienced investors to match down payment strategies with the right loan type, whether that is a fixed-rate, FHA, VA, or adjustable-rate mortgage. The pre-approval process gives you a realistic budget before you make any commitments, so your down payment decision is grounded in real numbers. Rileychase also walks you through popular loan options that fit a range of down payment levels, so you are not forced into a one-size-fits-all approach. Reach out to Rileychase today and get a clear, personalized plan that protects your cash reserves and puts you in the strongest possible position to buy.

FAQ

What is a down payment on a home?

A down payment is the upfront cash you pay toward a home’s purchase price at closing. It reduces your loan balance and directly affects your monthly payment, interest rate, and PMI requirement.

How much should I put down on a house?

The right amount depends on your savings, monthly budget, and financial goals. A 20% down payment eliminates PMI, while 10% offers a balance between lower payments and preserved cash reserves.

Does a larger down payment guarantee mortgage approval?

A larger down payment strengthens your application and reduces lender risk, but approval also depends on your credit score, income, and debt-to-income ratio.

What is PMI and when can I remove it?

PMI is private mortgage insurance required when your down payment is below 20%. You can request removal once you reach 20% equity through principal payments or home appreciation.

Is it better to wait and save a bigger down payment?

Not always. If home prices and interest rates rise while you wait, the total cost of the home can increase more than the savings you gain from a larger down payment.

Recommended

Related Posts