Discover why pre-approval strengthens your purchase offer. Gain a competitive edge in home buying with a credible, lender-verified offer.

Why Mortgage Points Matter for Home Buyers

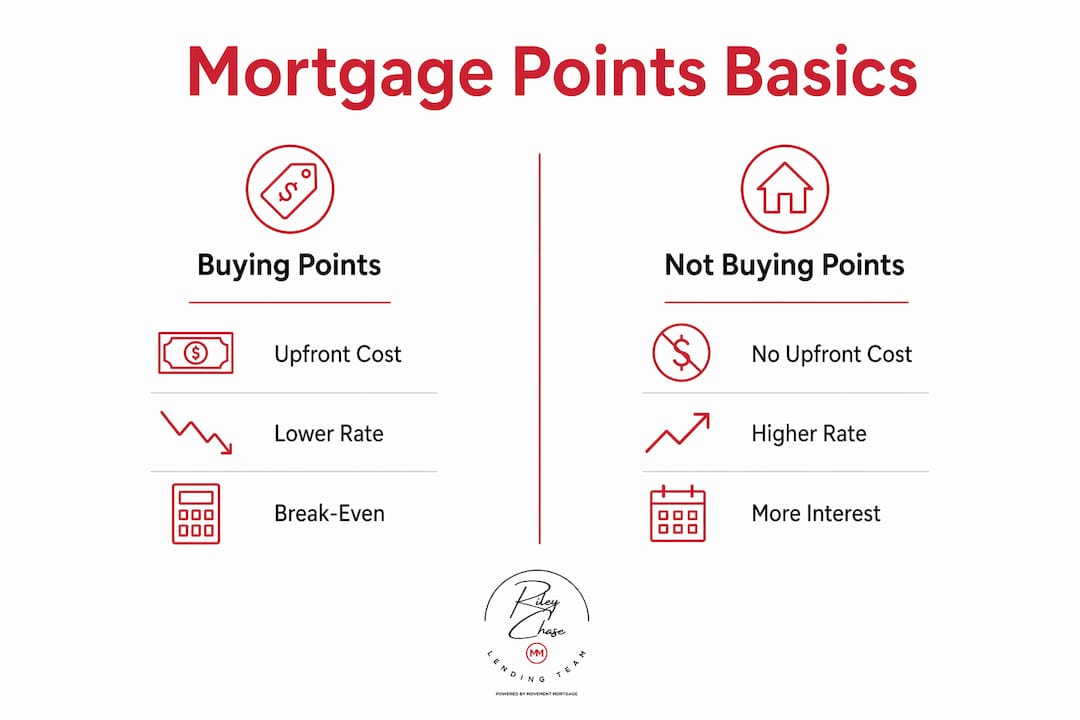

Mortgage points are prepaid fees you pay at closing to permanently lower your mortgage interest rate. Also called discount points, they are a form of prepaid interest recognized under IRS guidelines, which allow deductions under specific conditions when buying a primary residence. Understanding why mortgage points matter for buyers comes down to one question: how long do you plan to stay in the home? The answer determines whether paying upfront saves you thousands or costs you more than you gain.

How mortgage points affect loan costs and monthly payments

One mortgage point costs 1% of your loan amount and typically reduces your rate by 0.25%. On a $300,000 loan, that means paying $3,000 upfront to shave a quarter point off your rate. The savings feel modest month to month, but they compound significantly over a 30-year fixed mortgage.

The math becomes clearer when you look at the break-even point. Paying $3,000 for one point and saving $48 per month means you recoup that cost in 63 months. That is just over five years. Stay in the home longer, and every month after that is pure savings.

Not every lender structures points the same way. Some lenders allow fractional points, letting you buy 0.5 or 1.5 points rather than whole numbers. Lenders may permit purchases from fractions up to four points, giving you flexibility to fine-tune your rate reduction. Always ask your lender exactly how many points they offer and what rate reduction each point delivers.

The table below shows how points scale across different loan sizes on a 30-year fixed mortgage, assuming a 0.25% rate reduction and $48 monthly savings per point.

| Loan Amount | Cost of 1 Point | Monthly Savings | Break-Even (months) |

|---|---|---|---|

| $200,000 | $2,000 | ~$32 | ~63 |

| $300,000 | $3,000 | ~$48 | ~63 |

| $400,000 | $4,000 | ~$64 | ~63 |

| $500,000 | $5,000 | ~$80 | ~63 |

The break-even period stays consistent because both the cost and the savings scale proportionally with the loan amount. What changes is the total dollars at stake.

Pro Tip: Divide the total cost of your points by your monthly savings to find your personal break-even month. If you plan to move or refinance before that month, skip the points.

Do mortgage points actually save money?

Mortgage points save money only when you keep the loan long enough to pass the break-even threshold. Points are prepaid interest tied to the life of the loan. Refinance or sell before month 63, and you walk away having paid for savings you never collected.

The decision gets more complicated when you factor in your down payment. Using cash to buy points instead of increasing your down payment can push your loan-to-value ratio above 80%. That triggers private mortgage insurance, which adds a monthly cost that can easily cancel out the rate savings. Run both scenarios before committing.

Here are the key pros and cons buyers should weigh:

Benefits of buying points:

- Permanently lower interest rate for the life of the loan

- Reduced monthly payments that free up cash flow

- Potential tax deduction under IRS guidelines for primary residences

- Improved debt-to-income ratio, which can help you qualify for a larger loan

Risks of buying points:

- Upfront cash outlay reduces funds available for down payment or reserves

- Savings evaporate if you refinance or sell before break-even

- May trigger PMI if down payment drops below 20%

- Rate environment shifts can make refinancing attractive before you recoup costs

Pro Tip: Model your scenario with and without PMI before buying points. A mortgage professional can run both calculations side by side so you see the true net savings.

How do market conditions influence buying points?

High interest rate environments increase the value of buying mortgage points. When prevailing rates are elevated, locking in a lower rate through points delivers larger absolute savings over time. A 0.25% reduction on a 7% loan saves more total interest than the same reduction on a 4% loan.

When rates are expected to fall, the calculus shifts. Buying points to lock in a rate reduction makes less sense if you anticipate refinancing within two to three years to capture a lower market rate. You would pay the upfront cost and then refinance before reaching break-even.

Use these four steps to evaluate market conditions before buying points:

- Check current mortgage rate forecasts. Review published outlooks from the Federal Reserve and major housing economists. If rates are projected to drop significantly, points carry more risk.

- Assess your refinancing likelihood. Be honest about whether you would refinance if rates fell by 1% or more. If yes, points are a poor bet in a declining rate environment.

- Calculate your debt-to-income ratio with and without points. A lower monthly payment from buying points can improve your DTI, which lenders use to determine loan eligibility.

- Compare the total interest paid over your expected ownership period. Use a mortgage calculator to model 5, 10, and 15-year scenarios. The numbers often tell a clearer story than intuition does.

Buyers who plan to stay in a home for a decade or more in a high-rate environment get the most value from points. Short-term buyers in a declining rate environment get the least.

Mortgage points vs. other home financing strategies

Mortgage points are one tool among several for reducing your long-term loan cost. The right choice depends on your cash position, your timeline, and your risk tolerance.

Using cash for a larger down payment reduces your principal immediately. That lowers both your monthly payment and your total interest without any break-even calculation required. It also keeps you above the 20% threshold that eliminates PMI. Buyers who are close to that 20% mark should prioritize the down payment over points in most cases.

Adjustable-rate mortgages offer lower initial rates without any upfront cost. The trade-off is rate uncertainty after the fixed period ends. For buyers who plan to sell or refinance within five to seven years, an ARM can outperform a fixed rate with points. For buyers who want long-term certainty, points on a fixed-rate loan deliver more predictable savings.

| Strategy | Upfront Cost | Monthly Savings | Break-Even | Best For |

|---|---|---|---|---|

| Buying points | High | Moderate | 5+ years | Long-term owners in high-rate markets |

| Larger down payment | High | Moderate to high | Immediate | Buyers near 20% threshold |

| Adjustable-rate mortgage | Low | High initially | N/A | Short-term owners |

| Shorter loan term | None | None (higher payment) | N/A | Buyers prioritizing equity growth |

No single strategy wins across every situation. Your goals and financial position determine the best fit. Buyers who plan to stay 10 or more years in a high-rate environment gain the most from points. Buyers with limited cash reserves should protect their down payment first.

Key Takeaways

Mortgage points reduce your interest rate permanently, but they only save money if you stay in the home past the break-even period, which typically runs about 63 months.

| Point | Details |

|---|---|

| Cost of one point | One point equals 1% of the loan amount and reduces your rate by about 0.25%. |

| Break-even timeline | Savings typically offset the upfront cost after roughly 63 months of payments. |

| PMI risk | Using cash for points instead of a down payment can trigger PMI and erase savings. |

| Market timing matters | High-rate environments make points more valuable; declining rates reduce their benefit. |

| Compare all strategies | Points, larger down payments, and ARMs each suit different buyer timelines and goals. |

What I’ve learned from watching buyers get this decision wrong

Most buyers treat mortgage points as a simple yes-or-no question. They either buy them because a lender recommends it, or they skip them entirely because the upfront cost feels uncomfortable. Both approaches miss the point.

The buyers I’ve seen benefit most from points share one trait: they did the math before closing, not after. They knew their break-even month, they modeled the PMI scenario, and they compared the points option against putting that same cash toward their down payment. That 20-minute calculation changed their decision in almost every case.

The most common mistake I see is buyers purchasing points while sitting just below the 20% down payment threshold. They pay $3,000 for a rate reduction and then spend $150 per month on PMI for years. The net result is negative. A mortgage professional can catch this in minutes, but only if you ask the right question: “What happens to my PMI if I use this cash for points instead of my down payment?”

Mortgage points are a genuine financial tool, not a sales add-on. But they require honest answers about how long you plan to stay, whether you might refinance early, and what your cash reserves look like after closing. Get those answers first, then decide.

— Riley

Rileychase can help you model your mortgage point decision

Choosing whether to buy mortgage points is a calculation, not a guess. Rileychase works with first-time buyers and experienced investors to run the exact numbers that make this decision clear.

Rileychase offers personalized loan comparisons across fixed-rate, adjustable-rate, FHA, and VA loans, so you can see how points interact with each loan type before you commit. The pre-approval process at Rileychase includes a full review of your financing options, including whether buying points makes sense given your timeline, down payment, and rate environment. You can also review popular loan options to understand how points fit within the broader picture of your home purchase. Reach out to Rileychase to get a clear, personalized breakdown before closing day.

FAQ

What are mortgage discount points?

Mortgage discount points are prepaid fees paid at closing to permanently lower your interest rate. One point costs 1% of the loan amount and typically reduces the rate by 0.25%.

Do mortgage points save money in the long run?

Points save money if you keep the loan past the break-even period, which is typically around 63 months. Selling or refinancing before that point means you paid more upfront than you recovered in savings.

Can mortgage points be deducted on taxes?

IRS guidelines allow deducting points under specific conditions when buying or improving a primary residence. Consult a tax professional to confirm eligibility for your situation.

Should I buy points or increase my down payment?

Buyers close to the 20% down payment threshold should prioritize the down payment. Dropping below 20% to fund points can trigger PMI costs that cancel out the rate savings.

How do I know if buying points is right for me?

Calculate your break-even month by dividing the total points cost by your monthly savings. If your planned ownership period exceeds that number, points are likely worth it.

Recommended

- How Rising Interest Rates Impact Your Homebuying Power – Movement Mortgage

- The Impact of Higher Mortgage Rates: What Homebuyers Need to Know – Movement Mortgage

- 5 Crucial Questions to Ask a Mortgage Professional Before Buying a Home – Movement Mortgage

- Decoding Current Mortgage Rates: What Homebuyers Need to Know – Movement Mortgage

Related Posts