Discover how mortgage lender profit works and how it impacts your home loan fees and terms. Get the insights you need to make informed decisions.

Why Refinancing Resets Your Loan Term: A Clear Guide

Refinancing resets your loan term because it replaces your existing mortgage with a brand-new loan that starts its own repayment schedule from scratch. This process, known in the industry as loan term reset or amortization restart, is the core reason why refinancing resets loan term calculations for millions of homeowners each year. Your new loan defaults to a fresh term between 8 and 30 years, with 30 years being the most common choice. Understanding this mechanic before you sign protects you from paying far more interest than you planned.

Why refinancing resets your loan term: the mechanics explained

When you refinance, your lender pays off your old mortgage completely. A new loan takes its place, and that new loan carries its own amortization schedule starting at month one. The repayment clock does not continue from where your old loan left off. It starts over.

Amortization is the process of spreading your loan payments across the full term. Early in any amortization schedule, most of each payment goes toward interest rather than principal. Refinancing returns you to this front-loaded phase, which means your equity builds more slowly in the early years of the new loan.

Here is a concrete example. Say you are 8 years into a 30-year mortgage. You have 22 years left. You refinance into a new 30-year loan. Your remaining term just jumped from 22 years back to 30. You are now scheduled to pay off your home 8 years later than your original plan.

The term length you choose at refinance directly shapes your new amortization schedule. Your options typically include:

- 30-year fixed: Lowest monthly payment, most interest paid over time

- 20-year fixed: Moderate payment, meaningful interest savings

- 15-year fixed: Higher monthly payment, fastest payoff and lowest total interest

- Custom terms (8–29 years): Match your remaining original term or set a specific payoff date

Pro Tip: Ask your lender to match your new loan term to the years remaining on your current mortgage. If you have 22 years left, request a 22-year term. Many lenders offer custom terms, and Rileychase can walk you through exactly which options fit your situation.

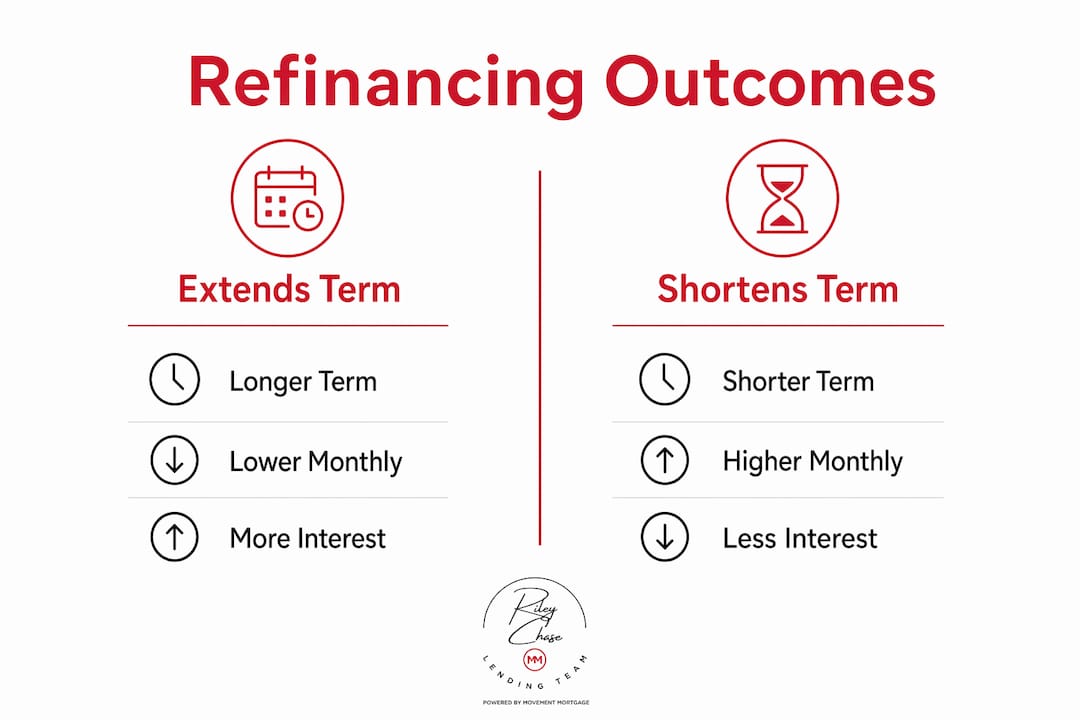

Does refinancing always extend your total repayment period?

Refinancing does not automatically extend your total repayment period. The outcome depends entirely on the term you choose for your new loan.

The table below shows how the same refinance decision produces very different timelines depending on term selection.

| Scenario | Original term remaining | New loan term | Net change in payoff timeline |

|---|---|---|---|

| Refinance into 30-year | 22 years | 30 years | +8 years longer |

| Refinance into 20-year | 22 years | 20 years | 2 years shorter |

| Refinance into 15-year | 22 years | 15 years | 7 years shorter |

| Match remaining term | 22 years | 22 years | No change |

Resetting to a 30-year term after 8 to 10 years into your original mortgage adds years to your repayment timeline and increases total interest paid over the life of the loan. That is the most common mistake homeowners make without realizing it.

Choosing a shorter term does the opposite. Refinancing from a 30-year to a 15-year term cuts years off your loan and reduces total interest, but it raises your monthly payment. The right choice depends on your cash flow today versus your total cost over time. Both are real numbers worth calculating before you commit.

Financial impact of resetting your loan term

The most visible effect of a loan term reset is a change in your monthly payment. A longer term lowers the payment. A shorter term raises it. But monthly payment is only one part of the picture.

Total interest paid over the life of the loan is the number that truly measures the cost of refinancing. A lower rate on a longer term can still cost you more in total interest than your original loan would have. This is why borrowers often miscalculate refinancing benefits by focusing solely on monthly savings and ignoring the full lifetime cost.

Closing costs add another layer to the calculation. Refinancing typically costs 2%–5% of the loan amount in closing fees. Experts generally recommend a rate reduction of at least 0.75% to break even within roughly 3 years. That break-even point is the minimum threshold for refinancing to make financial sense.

| Factor | Lower monthly payment | Lower total interest |

|---|---|---|

| Best loan term | Longer (30-year) | Shorter (15-year) |

| Monthly payment | Lower | Higher |

| Total interest paid | Higher | Lower |

| Break-even timeline | Longer | Shorter |

Rolling closing costs into the new loan balance is a common shortcut, but it carries a real cost. Financing closing costs means you pay interest on those fees for the full life of the loan, which increases your total borrowing cost. Paying closing costs out of pocket at closing is almost always the cheaper option if you have the funds available.

Pro Tip: Use a break-even calculator before finalizing any refinance. Divide your total closing costs by your monthly savings to find your break-even month. If you plan to move before that date, refinancing likely costs you money.

Refinancing strategies to avoid unwanted loan term resets

You have real control over how refinancing affects your loan period. The key is making deliberate choices rather than accepting the default 30-year term your lender may present first.

The most effective strategies include:

- Choose a term that matches or beats your remaining balance. If you have 18 years left, ask for an 18-year or 15-year loan. This keeps your payoff date on track or moves it closer.

- Make extra principal payments after refinancing. Even if you take a 30-year term for the lower payment, paying extra each month toward principal shortens your actual payoff date without locking you into a higher required payment.

- Understand cash-out refinance implications. Cash-out refinancing almost always resets to a 30-year term because the loan amount increases and lenders want longer repayment windows. If you take cash out, plan for a full term reset.

- Align your refinancing goal with your financial plan. Refinancing for a lower rate is different from refinancing to access equity. Each goal carries a different optimal term length.

- Avoid serial refinancing. Serial refinancing into new 30-year loans is a common driver of long-term mortgage debt extension. Each reset compounds the total interest you pay across your homeownership years.

Exploring your types of mortgage refinancing options before you apply gives you a clearer picture of which path fits your goals. Rate-and-term refinancing, cash-out refinancing, and streamline refinancing each affect your loan period differently.

Key Takeaways

Refinancing resets your loan term because it creates a new loan with a fresh amortization schedule, and the term you choose at that moment determines whether you pay off your home sooner, later, or on the same timeline as before.

| Point | Details |

|---|---|

| Term reset is automatic | Every refinance replaces your old loan and restarts the amortization clock from month one. |

| 30-year default adds years | Refinancing into a new 30-year loan after years into your original mortgage extends your payoff date. |

| Shorter terms save interest | Choosing a 15-year or 20-year term at refinance reduces total interest, though monthly payments rise. |

| Closing costs matter | Typical closing costs run 2%–5% of the loan amount; a 0.75% rate drop is the common break-even threshold. |

| Cash-out resets fully | Cash-out refinancing almost always triggers a full 30-year term reset due to the increased loan balance. |

What I’ve learned from watching borrowers reset their loans

Most homeowners I talk to come to refinancing with one question: “Will my monthly payment go down?” That is a fair question. But it is the wrong first question.

The right first question is: “How much will this loan cost me in total?” A refinance that saves $200 a month but adds 8 years to your mortgage can cost you tens of thousands of dollars more over time. The monthly savings feel real and immediate. The extra years of interest feel abstract until you do the math.

The pattern I see most often is what I call the serial reset trap. A homeowner refinances at year 7 into a new 30-year loan. Then at year 5 of that loan, they refinance again into another 30-year loan. Twelve years into homeownership, they are still looking at 30 more years of payments. Their mortgage has become a permanent fixture rather than a debt they are paying down.

The fix is straightforward. Match or shorten your term at every refinance. If you need the lower payment of a longer term, make extra principal payments to compensate. And always calculate your break-even point before signing. Rileychase builds this kind of personalized refinancing guidance into every client conversation, because the numbers tell a story that the monthly payment alone never does.

— Riley

Rileychase helps you refinance with confidence

Refinancing is one of the most consequential financial decisions you will make as a homeowner. The term you choose shapes your monthly budget and your total cost for years to come.

Rileychase specializes in helping homeowners and first-time buyers understand every dimension of their refinancing options, from term length selection to break-even analysis. Whether you are considering a 15-year vs. 30-year mortgage or exploring cash-out options, the team at Rileychase walks you through the real numbers before you commit. Start with a pre-approval conversation to understand your options and build a refinancing plan that fits your financial goals, not just your monthly budget.

FAQ

Why does refinancing reset the loan term?

Refinancing replaces your existing mortgage with a new loan that carries its own amortization schedule and term length. The old loan is paid off completely, so the repayment clock starts over from month one.

Does refinancing always extend my mortgage?

No. Refinancing extends your mortgage only if you choose a term longer than your remaining balance. Selecting a shorter term, such as a 15-year loan, can actually shorten your total repayment period.

How does refinancing affect total interest paid?

Refinancing resets you to the front-loaded interest phase of amortization, where early payments go mostly toward interest. Choosing a longer term increases total interest paid; a shorter term reduces it.

What closing costs should I expect when refinancing?

Closing costs typically run 2%–5% of the loan amount. Most financial experts recommend a rate reduction of at least 0.75% to break even on those costs within about 3 years.

Does a cash-out refinance always reset my loan term to 30 years?

Cash-out refinancing almost always resets the loan term to 30 years because the increased loan balance requires a longer repayment window from the lender’s perspective.

Recommended

Related Posts